ECUADORIAN GROUP ORGANISATION LOGO

ECUADORIAN GROUP ORGANISATION LOGO |

The Company Aymesa is a corporation organized

and existing under the laws of the Republic of

Ecuador.

-Over 88 percent of the total shares outstanding

are owned by two (2) investor groups composed

of Ecuadorian nationals:

-The Eljuri Group

-Invelei (Employee Holding Company)

-There are no automotive manufacturers associated

with or holding equity participation in the company.

-The Company Aymesa is a corporation organized

and existing under the laws of the Republic of

Ecuador.

-Over 88 percent of the total shares outstanding

are owned by two (2) investor groups composed

of Ecuadorian nationals:

-The Eljuri Group

-Invelei (Employee Holding Company)

-There are no automotive manufacturers associated

with or holding equity participation in the company.

|

Company Vision |

As a Company we believe on:

*-Build achievable objectives

-Maintain a healthy business.

-Comply our commitments.

-Be an innovative and fearless competitor in the

marketplace

-Build an strong brand image

-Ensure dealer's profitability

-Long term planning

* As a company we will not:

-Work in anyway different that the best way that

guarantees our success

in the future.

|

Our products |

Automobiles:

|

Long term Objective |

Ecuadorians Caracteristics- Main Country Caracteristic

Population: 12'646.093 inhabitants

* Registered cars: 667.494

* Cars per 100 inhabitants: 5.2

* Automotive market: 30 brands & 275 models

* Market dominated by GM : 47.2% (Year 2002)

* Second brand Hyundai: 8.1% (Year 2002)

* Third brand KIA: 6.5% (Year 2002

|

International vision |

In Ecuador and Colombia Aekia and Metrokia are

strongly allied together. with

Having the common objective of fully participating

in the development of Kia Motors into one of the

top five international automotive companies in

the world by the year 2010.

|

AEKIA VISION |

AEKIA S.A. will become the number 2 company in

the Ecuadorian automotive market by the year 2010

(15%Market Share)

|

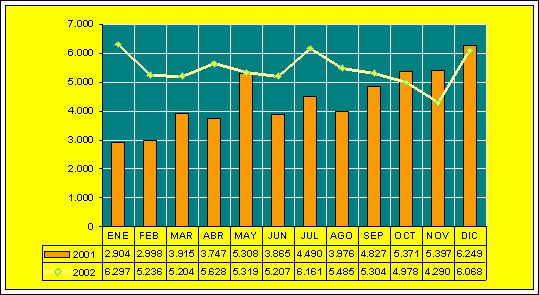

Evolution 2001-2003 |

EVOLUTION 2001-2003 CHART

Table

* Shown chart graphically illustrates the cyclical

nature of the Ecuadorian Automotive Market.

* The opening in 1992 of a long closed market

resulted in a grand surge in sales reaching its

peak in 1994.

* Similarly in 1999 a series of bank failures

lead to a lack of consumer confidence and a subsequent

dramatic fall off in automotive sales.

* During the year 2000 automotive sales rebounded

to about 50% of normal volume.

* Calendar year 2003 Automotive Sales are expected

to reach more normal market levels in the area

of 40/45,000 units.

|

|

KIA Brand Background |

* The Kia brand had been abandoned. The market

place had not been supplied with Kia product for

more than two (2) consecutive years.

* The Kia brand was unknown with no level of recognition

in the mind of the public. There was no residual

value left in the brand.

* Former customers complained of lack of service

for their vehicles and a deficiency in the supply

of service parts.

* There was no exclusive point of sale for the

display, sale and service of Kia vehicles.

* The image of the brand was further damaged by

the poor design and quality of dealership facilities

and signage.

*During the six (6) year period under review GM

maintained its strong leadership role with Toyota

and Volkswagen lagging far behind in second and

third place respectively.

* Both Hyundai and Daewoo, also maintained a significant

presence during this period appearing regularly

in the top ten.

* However, Kia has been mostly dormant during

this period and made no sales during calendar

years 1999 and 2000.

* Under the new franchise holder (Aekia S.A) Kia

is Showing a strong recovery in calendar year

2001.

KIA BRAND PERFORMANCE

2002 RESULTS FOR THE YEAR |

* Year 2002 was the sales record of all automotive

industry in Ecuador overpassing 1994 figures.

* Industry volume grew 23% in 2002 vs. 2001 as

compared with KIA that grew 162% in sales volume

in the same period.

* GM maintained its leadership with two large

promotions based on retail price reduction.

* Large offerings within automobile and passenger

van segments has changed some habits and attitudes

from consumer towards SUV.

MARKET SHARE

* 2001 From 0% to 3.1%

* 2002 From 3.1% to 6.5%

* From 0 position to 9th in Dec 2001

* From 9th to 3rd in Dec 2002

GROWTH

* Fastest growing brand since its launching on

Feb/01.

* Aggressive and fearless competitor

* Compete aggressively in the 2 major segments

in the market and created

new passenger van category

DEALER NETWORK

* Development of 15 points of sale in a short

period of time

* Presence in 99% of the country's automotive

market sales.

* All KIA dealers are 3 in 1 and give a solid

and impressive image

* CSI: Dec 01: 82. 3pp over SA avg and 9 pp over

worlwide avg. CSI:

Dec 02: 84/100 or 4.2/5 for costumers after1 year

of purchase.

RANKING BY SEGMENT

* Pregio Leader

* Sportage 3rd position

* Carens 2nd position

* Rio & Spectra 6th position

* Carnival Low volume/brand image

* K2700II Almost only offer in a reduced segment.

|

WHAT IS KIA NOW? |

* 6.899 units sold up to date (03-03).

* KIA brand growth of 162% in sales volume as

compared with year

2001 within an industry that grew 23% .

* Double the market share of year 2001, from 3.1%

to 6.5% market Share

up to date (12-02). (23 months from launching)

* Improvement of brand ranking position from zero

in year 2000 to 3rd

up to date (12/02).

* Increased Top of Mind Awareness: From 0.5% (05/01)

to 10.2% (12-

02)

* Heavy advertising support thus creating KIA

ad awareness at 53.6%

level (12-02)

* First recall of Kia advertising rose from: 0.2%

to 14.3% (12-02).

Strong advertising becoming the second investor

among the automotive industry while building strong

brand image: Total Brand Awareness 85.3% (12-02).

* Aggressive launching of 7 new models during

the year: New Carnival, Rio RS version, Carens

and Rio F/L, Spectra N/B, Spectra HB, and Sorento.o

Development of a well structured and extensive

dealer network (3 in 1) completing 15 points of

sales covering cities that represent 99% of the

total automotive market volume.

* Improved brand penetration mainly within automobile

segment through Rio sales strengthening and Spectra

launching reaching a projected 4.35 % of market

share within this market segment by the end of

year 2002. Last 3 months average reached 6.4%

in year 2002 as compared with a poor 0.3% of total

year 2001.

|

Dealer Network Development |

|

{kind=link}