77

Investment & Legal Framework

sponsible for the formulation of the country’s tax policy,

and the implementing agency is the Zambia Revenue

Authority (ZRA). The legislative framework relating to

the regulation and administration of the tax system

is provided in the Income Tax Act, 1966. The exact

amount an individual pays in taxes is based on one’s

income and home of residence.

The tax year runs from 1 January to 31 December.

Taxpayers are generally expected to adopt 31 March

as their accounting date, and ZRA’s prior approval is

required for taxpayers to adopt a different accounting

date. Any change in the accounting date also requires

prior approval from ZRA.

The ZRA requires taxpayers to submit annual tax re-

turns—including accounts and supporting schedules—

on or before 30 September. There are penalties for late

submission of tax returns on or before the stipulated

date.

The principal taxes include direct taxes, customs and

excise duties, the value added tax (VAT), property

transfer taxes, and mineral royalties (Mines and Miner-

als Act, 1995).

Corporate Tax

The Zambia Revenue Authority levies corporate taxes

at the rate of 35%. Income from the agricultural sector

and non-traditional exports (all exports except copper

and cobalt) is levied at 15%, while companies listed on

the Lusaka Stock Exchange are taxed at the rate of

33%. Banks with incomes in excess of K250 million are

levied a corporate tax at the rate of 40%.

Personal

Income Tax

This tax is levied in the range of 25-35%. The maxi-

mum rate applicable to farmers is 15%.

Employers are required to register and operate a Pay-

As-You-Earn (PAYE) scheme under which they are re-

quired to deduct the appropriate tax from the sala-

ries of its employees. They must then remit the tax

to the Zambia Revenue Authority.

Doubl

e Taxation Ag

reements

Some eligible taxpayers find themselves liable to

be taxed in more than one country or territory. The

predicament of international double taxation can

adversely affect the international flow and mobil-

ity of human, financial, and investment resources;

therefore, the international community has de-

vised a mechanism to mitigate the incidence of

double taxation.

The countries that Zambia has signed Double Tax-

ation Agreements include the following: Canada,

Denmark, Finland, France, Germany, Holland,

India, Ireland, Italy, Japan, Kenya, Mauritius, Nor-

way, Romania, South Africa, Sweden, Tanzania,

Uganda, United Kingdom, Yugoslavia, and Zim-

babwe.

INVESTMENT CLIMATE

The Zambia Development Act assures investors

that property rights are respected. No investment

of any kind can be expropriated unless the Parlia-

ment has passed an act relating to the compul-

sory acquisition of that property. Also, in case of

expropriation, full compensation shall be made at

market value and shall be convertible at the cur-

rent exchange rate.

In addition to being a member of a number of in-

ternational agreements, Zambia is part of the Mul-

tilateral Investment Guarantee Agency (MIGA) of

the World Bank. This guarantees foreign invest-

ment protection in cases of war, strife, disasters,

etc.

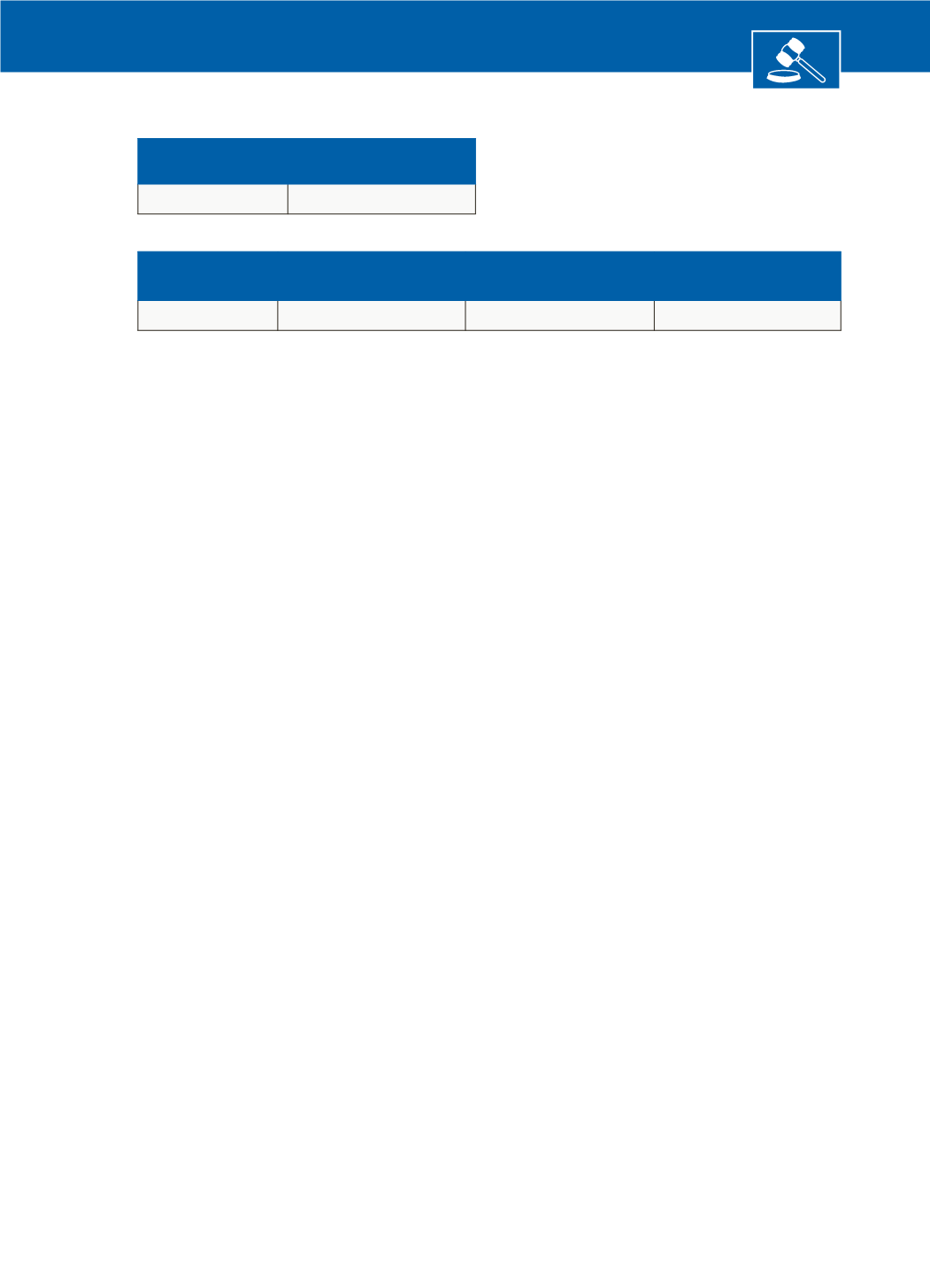

Corporate Tax Rate

Normal

Tax

Rate

Bank

s w

ith income

ov

er K2

5

0

mil

l

ion

Lusak

a Stock

Exchang

e

companies

Ag

ricul

tural

companies

3

5

%

40%

33%

15%

Personal

Income Tax Rate

Normal

Tax Rate

Farmers exemption

2

5

%

- 3

5

%

15% maximum