Sector Structure

Sector Structure |

Sonelgaz's monopoly on electricity distribution,

generation and transmission came to an end in January

2002, when new legislation was passed to open up

the gas and power sectors. Under the terms of the

new law, independent electricity and gas regulatory

bodies will be established during a three-year transition

period ahead of the sale of a 30% stake in the company.

The sale will herald the opening-up of the electricity

and gas sectors to private investment, and Sonelgaz

is also to be restructured during the transition

period into two shareholding companies - one to

cover electricity generation and supply, the other

responsible for gas distribution. The regulatory

bodies will ensure basic technical standards and

fair competition. Sonelgaz had previously been given

permission to negotiate build operate own (BOO)

deals with foreign operators.

The first such project calls for a 2,000 MW power

station to be built, 400 MW of which would be purchased

by Sonelgaz for domestic supply with the remainder

to be exported. Work is progressing on joining the

power grids of Libya, Tunisia, Morocco and Algeria.

Sonelgaz will retain a monopoly on the domestic

transmission network. The proposed BOO schemes have

so far met with some interest from foreign investors,

but companies have been awaiting clarification of

the legal framework under which the project would

operate before committing to any deal.

|

Generation |

Algeria has a current electricity generating capacity

of approximately 5,000 MW with demand growing at

5% annually. The state-owned utility Sonelgaz has

a monopoly on electricity generation which is now

set to end following a decision to encourage build-own-operate

(BOO) schemes. The decision to open up the generation

sector to foreign investors (most likely through

partnership with Sonelgaz) came in 1998, against

a background of falling government oil revenues

(due to the price slump).

|

Renewables |

Sonatrach set up a renewable energy joint venture

company with Sonelgaz, and the agricultural food

group Semouleries Industrielles de la Mitidja (SIM)

in July 2002. The new company, which is jointly-owned

by the three companies (Sonatrach - 45%; Sonelgaz

- 45%; SIM - 10%) will be called New Energy Algeria

(NEAL), and will be tasked with developing photovoltaic,

wind, solar and biomass energy production within

Algeria.

|

Transmission, Distribution and Marketing |

Transmission, Distribution and Marketing

Sonelgaz was made a joint stock company in 1999

and was split up under the terms of the 2002 power

law. The move should enable the company to seek

alternative sources of capital and form partnerships.

The government has taken a strategic decision to

make Sonelgaz more competitive, but has stopped

short of full power-sector privatisation, with Sonelgaz

to retain a monopoly on distribution and transmission.

Sonelgaz and Sonatrach announced an agreement to

set up a joint company to explore investment opportunities,

foreign and domestic, in the electricity and gas

sector. The agreement indicates Algerian state-owned

firms will seek wider commercial opportunities.

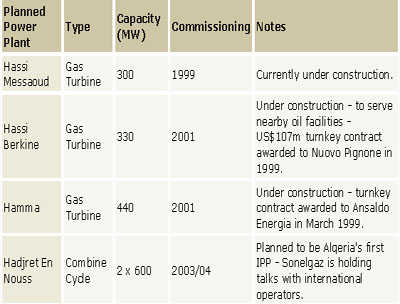

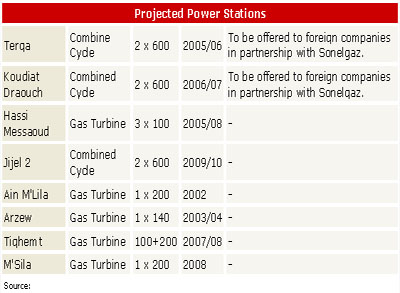

The announcement of several generation projects

(see table below) open to foreign investors has

so far met with little interest from foreign investors.

Legal and implementation clarifications have been

sought by companies before they will seriously consider

the projects. Sonatrach has already awarded the

first privately-funded power plant contract to Nuovo

Pignone for the construction of a 330 MW gas turbine

plant at Hassi Berkine.

Sonelgaz opened technical bids submitted for the

construction of a 2,000 MW independent power plant

(IPP) at Skikda (Hadjret En Nouss), on 31 January

2001. The terms of the IPP will see 800 MW of power

being purchased by Sonelgaz for domestic consumption,

with the remainder targeted for export to southern

Europe, to be marketed by Sonelgaz and the winning

company. The transit of electricity to Italy, France

and Spain may involve the construction of a direct

undersea link, but transit through Tunisia and Morocco

has not been ruled out. Five companies eventually

submitted technical bids for the US$1,500m-US$2,000m

build operate own (BOO) project: Spanish company

Endesa, Enelpower of Italy, Electricite de France,

AES corporation of the US and SNC Lavalin from Canada.

Commercial bids will then be submitted once a feasibility

study into a power link to Spain has been completed.

The strong backing for the project from the World

Bank has boosted the confidence of the developers.

Table

Planned Power Stations

Table

Projected Power Stations

(Make

a click here)

Excellent demand for alger energy 2003

A very competitive and promising business environment

on the Algerian energy, petrochemical, mining and

electricity market leads to an excellent demand

for alger energy 2003. With revenues of about US

$ 20 billion, this sector creates 35% of the Algerian

GDP, 97% of export revenues and 65% of the overall

state budget. According to the Algerian ministry

of energy and mines, huge investments are being

realised during the years 2000-2010. US $ 22 billion

are being invested in the petrochemical sector alone,

and US $ 12.2 billion in the field of electricity

and the distribution of oil and gas.

On the Algerian gas export strategy, Neil Ford writes

in 'Oil Review Middle East', Issue Two 2003:

'Algeria is ideally located to make the most of

the EU's liberalised gas markets. A massive 90 per

cent of all Algerian gas production is already exported

to the European Union. The Algerian government has

set about restructuring its energy sector. The downstream

gas and power sectors have already been liberalised

through legislation passed in February 2003, which

allowed for independent power producers (IPPs).

Foreign oil and gas companies remain enthusiastic

about the planned reform. The nuts and bolts of

Algeria's gas export strategy are impressive. The

country possesses the seventh biggest proven gas

reserves in the world at 159,700 billion cubic feet.

Algeria is firmly in the driving seat when it comes

to making the most of increasing EU demand. It possesses

the longest established LNG sector, is the best-connected

North African country to Europe via pipelines and

is geographically the best located. With the current

reform and liberalisation of the country's energy

sector making good progress, the government can

look forward to growing gas revenues, which should

help reform the rest of the economy.'

On this background it comes with no surprise that

the demand to participate at alger energy 2003 is

excellent. UBI France, the French Agency for International

Business

Development, have already registered with 180 sqms

for an official French pavilion. A Russian and Ukrainian

pavilion at alger energy 2003 is being organized

by Negus Expo, Moscow and an official Canadian pavilion

is put together by the Canadian embassy in Algiers.

Apart from those official group participations,

many individual exhibitors, who participated at

the launch event of alger energy in 2002 with smaller

stands, are now showing off, such as ABB and Schneider

Electric.

Of course Sonatrach and Sonelgaz are again in with

huge stands as well as AEC, Aksa, Amerada Hess,

Dragados, Gaz Inter, Great, Groupement Transformateurs,

Solar Turbines, Siraga, Stroytransgaz, Vatech, Vectra

and many others.

With his letter of 3 March 2003, the minister of

energy and mines, Mr. Chakib Khelil officially puts

alger energy 2003 under his auspices and invites

"all of our partners to participate at this

important event." "The prospects for business

in Algeria are very promising", writes the

minister and sees alger energy 2003 on a good way

to become "the most important annual gathering

in North Africa on energy, mining, petrochemicals

and electricity."

The 2nd international energy, mining, petrochemical

and electrical engineering trade fair of Algeria

- alger energy 2003 - is scheduled to take place

at the Palais des Expositions, Pins Maritimes, Algiers

from 28 September - 01 october 2003. alger energy

is again organized by fairtrade, in close cooperation

with the Algerian ministry of energy and mines and

with Safex, the leading Algerian trade fair organizer.

alger energy 2003 will again be the best platform

for all of the leading players in the Algerian market

to introduce new products, to network with traditional

customers and to make new business contacts. |

alger energy 2003 is

held in conjunction with the 10th Mediterranean

Gas Conference, which is held at the Hilton Algiers

on 30thSeptember and 1st October 2003, Day 3 and

Day 4 of alger energy 2003. This conference is organised

by Overview Conferences in association with Sonatrach

and it also enjoys the patronage of the Algerian

minister of energy.

ITOCHU Corporation and Ishikawajima-Harima Heavy

Industries Co., Ltd. (IHI) have jointly received

an order for a large-scale desalination/power generation

plant from Kahrama SpA, an Independent Water and

Power Producer (IWPP), as the first private business

in Algeria, and a contract was signed in Alger in

the presence of Mr. Khelil, the Minister of Energy

and Mines. The amount of contract is equivalent

to about 40 billion JPY. The contract is a full

turnkey contract which includes the engineering,

procurement, construction, installation, and performance

test of the plant. The plant will be completed by

the end of June, 2005.

Kahrama SpA, owned by BLACK & VEATCH and ALGERIAN

ENERGY COMPANY (a joint venture owned by the Algerian

state-own companies, SONATRACH and SONELGAZ, on

a 50-50 basis) will construct the first large-scale

desalination/power generation plant in the Arzew

industrial zone which is located in the vicinity

of Oran, the second biggest city in Algeria along

the Mediterranean sea.

This project includes construction of natural-gas

power generation facilities having an output of

320,000 kW, and facilities to desalinate seawater

using exhaust heat from the power plant (daily production:

approx. 88,000m3). It is decided that SONATRACH

and SONELGAZ will draw all output of water and electricity

over the next 25 years. The project aims to increase

the output of power generation in Arzew, which serves

as an industrial base in Algeria, and to replenish

water shortages in Oran caused by its population

increase and low rainfall, while using water as

industrial water.

In 1982 and 1998, ITOCHU and IHI constructed world-class

LPG Complex (annual production: 6-million tons)

in the areas adjacent to the construction site in

the Arzew industrial zone. Further, IHI has a track

record of supplying 20 desalination plants, as well

as power generation facilities, throughout the Middle

East. The IHI's experience leads to the order this

time.

Establishment of many IWPPs and desalination plants

are now being planned in the Middle East. Both companies

will keep focusing on the business activities in

this area.

|

Project Outline |

1. Client Name: Kahrama SpA

This company is a JV, 80% owned by BLACK & VEATCH,

and the remaining 20% owned by ALGERIAN ENERGY COMPANY

(AEC).

*AEC is an electric power company owned by the Algerian

state-own hydrocarbon public company, SONATRACH,

and state-own electricity public company, SONELGAZ,

on a 50-50 basis.

2. Site/Use:

Arzew industrial zone (about 350km westward from

Alger)

Meeting the demand for water and electricity in

various plants in the Arzew industrial zone and

the demand for water for civilian use.

3. Project Outline:

Contract Content: Full turnkey contract which includes

the engineering, procurement, construction, installation,

and performance test of the desalination/power generation

plant.

table

4. Competitors:

SNC-Lavalin of Canada and Enelpower of Italy.

5. IWPP:

Independent Water and Power Producer

THE 10 TH ANNUAL MEDITERRANEAN GAS CONFERENCE

IN ALGIERS

30 TH OF SEPTEMBER -1ST OCTOBER |

Introduction

Overview Conferences cordially invites you to attend

the 10th Mediterranean Gas Conference.We are delighted

to announce that this conference will be held in

Algiers, under the patronage of Dr. Chakib Khelil

and hosted by SONATRACH. The conference promises

to be a landmark event and the choice of Algiers

as a location reflects the central role that Algeria

continues to play in the rapidly changing and developing

Mediterranean gas business.Top level speakers from

all the key players in the Mediterranean industry

will meet in Algiers, to share information and debate

the future for the most exciting and varied gas

region in the world.To receive further details about

this important industry event: Email: events@economatters.com

or contact Kate Wright on Tel: +44 (0)20 7650 1402

Day Two - Wednesday 1st October 2003

Working Breakfast: Topic groups

Breakfast will be arranged in groups which will

discuss special themes. We will nominate and publicise

three topics but also invite new ones from delegates

Streamed Conference Sessions

Delegates have the choice of two conference streams

for the remainder of the morning

STREAM 4A: Institutional and Financial Aspects

Chairman:Khaled Boukhelifa

Director General, Ministry of Energy & Mines

Algeria

The European Union's programme for gas: security

of supply and the progress of liberalisation

Speaker from European Commission

STREAM 4B: Gas and Electricity Markets in Europe

and North Africa

Chairman:Aissa Abdelkrim BenghanemSonelgaz

The Algerian gas and electricity markets: demand

growth and market liberalisation

Madjid OthmaneDirector of Regulatory AffairsSonelgaz

How producing countries trade with liberalised

markets

Mr Abdullah Hussain SalattSenior Advisor to the

Minister of Energy and Industry, Qatar

Industry structure: the moves of the main players

David DrurySenior Associate, Gas Strategies

What role should international upstream companies

play in gas development?

David WalkerPresident, UK NA and ME Development

and Operations, BHP Billiton

How Mediterranean gas and power projects can

compete for international project finance:

Nobuyuki Higashi, Japan Bank for International Co-operation

- JBIC

Egypts Natural Gas Strategy: Transportation and

Treatment

Mahmoud LatifChairman, GASCO

How we will achieve the liberalisation of the

Turkish Gas Market

Yusuf GunayChairman, EMRA, Turkey

The pivotal role of the French market in southern

Europe gas and electricity

Speaker from Trading & Marketing, TotalFinaElf

The Iberian market: prospects for gas-fired power

generation

Pedro MoraledaDirector of International Relations,

Gas Natural

The Italian gas and electric ity markets

Speaker from Edison

Panel Session:

What are the lessons and key messages of the conference?·

Chairman: H.E. Dr. Chakib Khelil, Minister of Energy

and Mines, Algeria · Jean-Marie Dauger, Vice

President, Gaz de France · EU Representative*

· Ali Hached, Sonatrach · Aissa Abdelkrim

Benghanem, Sonelgaz · James Ball, Chairman,

Gas Strategies · Mr Abdullah Hussain Salatt,

Senior Advisor to the Minister of Energy and Industry,

Qatar

Mediterranean Policy Roundtable

Chaired by Sylvie Cornot-Gandolphe of the IEA

Delegates who are staying over in Algeria on Wednesday

night will have the opportunity to participate in

a roundtable which will explore the role of gas

in international policy in the Mediterranean. Members

of the diplomatic community in Algiers will also

be invited to the event, which will consider the

following themes: · Security and diversity

of supply · International trade and open

markets · Commonality of interest between

suppliers and buyers |

{kind=link}

{kind=link}

{kind=link}